Credit Card Statistics By Demographics, Types, Regional, Network And Issuers

Updated · Sep 25, 2024

WHAT WE HAVE ON THIS PAGE

- Introduction

- Editor’s Choice

- Credit Card Technical Specification

- Essential Credit Card Statistics

- Credit Card Demographics Statistics

- Types of Credit Card Interest Rate

- Credit Card Regional Statistics

- Credit Card Network and Issuers Statistics

- Credit Utilization Ratio Statistics

- Advantages and Disadvantages of Credit Card

- Conclusion

Introduction

Credit Card Statistics: A credit card is a card used to make payments, which a bank generally issues, and that allows users to purchase goods or services or withdraw cash on credit. Using the card, therefore, accrues debt that has to be repaid afterward. Credit cards are the most widely used form of payment in the world. A credit card is a charge card that needs the balance to be repaid in full every month or at the end of every statement cycle.

Credit cards also allow customers to build a debt balance that is related to the interest being charged. Let’s shed more light on “Credit Card Statistics” through this article.

Editor’s Choice

- Although 68% of US adults say that the US has enough savings to cover emergencies, the rest rely on other options. About 2% of US adults need to use a bank loan or credit line to handle unexpected costs.

- HDFC Bank leads the credit card market. As of March 2024, it holds the largest share.

- As of September 2023, the typical US household owes USD 6,568 on their credit cards.

- Wealthier households, specifically those in the highest income bracket, have a median credit card debt of USD 12,600, indicating that higher income is linked to higher credit card debt.

- According to Credit Card Statistics, this amount is roughly 3% higher than the average debt at the beginning of 2023.

- Most credit cards are 85.60 by 53.98 millimeters (3 3/8 inches by 2 1/8 inches) with rounded corners between 2.88 and 3.48 millimeters (9/80–11/80 inches).

- About 39% think they can clear their debt within the next year, and 24% estimate it will take two years. Around 5% expect to need five years, while 3% are still determining if they can pay off their debt at all.

- As of August 2023, Wisconsin has the lowest average credit card debt at USD 4,808. Iowa follows with an average debt of USD 4,811, and West Virginia has USD 5,005.

- The total credit card debt in the US will be USD 1.03 trillion by the second quarter of 2023, up from USD 1 trillion in the first quarter of 2023.

- In 2023, over 150 million cases of credit card fraud were reported in the U.S. AnoU.A frequent type of identity theft is the theft of federal documents.

- Debit card payments account for 10 out of every 35 transactions.

- As of March 2023, about 84% of US residents get credit cards to start improving their credit scores. This is especially common among Gen Z.

You May Also Like To Read

- Blockchain Statistics

- Cryptocurrency Statistics

- Phonepe Statistics

- Paypal Statistics

- Bhim App Statistics

- Online Payment Statistics

- Buy Now Pay Later Statistics

- Digital Banking Statistics

Credit Card Technical Specification

Most credit cards are 85.60 by 53.98 millimeters (3 3/8 inches by 2 1/8 inches) with rounded corners between 2.88 and 3.48 millimeters (9/80–11/80 inches). They are the same size as ATMs and other payment cards, like debit cards. Most are made of plastic, but some are made of metal.

Credit cards have a printed or embossed number that follows the ISO/IEC 7812 standard. The first part of this number called the Bank Identification Number (BIN), identifies the issuing bank and is the first six digits of MasterCard and Visa. The next nine digits are the account number, and the last digit is a check digit. These standards are set by ISO/IEC JTC 1/SC 17/WG 1. CW.G.dit cards have a magnetic stripe that meets ISO/IEC 7813 standards, and many now have a computer chip for extra security. Some advanced cards even include a keypad, display, or fingerprint sensor.

Credit cards also have issues, expiration dates, and extra codes, such as issue numbers and security codes. Some advanced cards offer changing security codes for safer online shopping. Different cards might have different sets of extra codes. Originally, card numbers and cardholder names were embossed to transfer information to charge slips easily. Now, with fewer paper slips in use, some cards are not embossed and may have the number on the back. Also, some cards are now vertical instead of horizontal.

Essential Credit Card Statistics

- In 2023, most credit card holders were Asian Americans (93%) and Caucasian Americans (88%).

- Visa, MasterCard, American Express, and Discover are the major credit card networks.

- Credit Card Statistics stated that Gen Z has the lowest average number of credit cards.

- In the US, the credit card market share is around 10.5%.

- By mid-March 2023, the average credit card interest rate was about 24.08%.

- Credit card utilization was recorded at 6% in 2023, with the average American having about three credit cards.

- According to Forbes, 98% of credit card users have an annual income of over USD 100,000.

(Reference: enterpriseappstoday.com)

- In the above pie chart, we can study how customers pay for their purchases.

- Visa holds about 71% of the global credit card market share. As of 2023, MasterCard has 24% of the global market share and 25.7% in the US.

- S 1% of US US card users with an income below USD 100,000 are likely to carry a month-to-month balance.

- As of February 2023, 32% of people use physical credit cards, while only 4% use virtual credit cards, which is lower than debit card usage, according to Credit Card Statistics.

- Credit cards are used by 96% of college graduates and 52% of high school students.

- In the second quarter of 2023, there were 578.35 million credit card accounts, a 5.2% increase from the previous year. Total credit card debt amounted to USD 1.031 billion.

- Around 14% of Americans use credit cards to pay their monthly bills, and nearly 49% have kept their primary credit card the same in the last five years.

- Chase is the top issuer of general-purpose credit cards in the US. Seven credit card issuers in the US made around USD 3.517 trillion in purchase volume last year.

- Debit cards remain the most preferred payment method, accounting for 10 out of 35 payments and 28% of card payments.

Credit Card Demographics Statistics

- Though people of any age can have credit card debt, the amount varies by age.

- According to Credit Card Statistics, the 55-—to 64-year-old and 65-—to 74-year-old age groups have the highest median credit card debt, at USD 3,500.

- The 55 to 64 age group also has the highest average credit card debt at USD 7,720.

- According to 2022 data from the Federal Reserve, Americans aged 45 to 54 are most likely to have credit card debt (57%), while those aged 75 or older are least likely (29.8%), as per Credit Card Statistics.

| Cardholder Age | Median Credit Card Debt | Average Credit Card Debit | Percentage with credit card debt |

75+ | USD 1,700 | USD 3,990 | 29.8% |

| 65-74 | USD 3,500 | USD 7,720 | 33.9% |

55-64 | USD 3,500 | USD 7,530 | 44.3% |

| 45-54 | USD 3,000 | USD 6,660 | 57.0% |

35-44 | USD 2,900 | USD 6,370 | 52.6% |

| 18-34 | USD 1,700 | USD 4,070 | 48.5% |

- Most households earning over USD 100,000 a year have a credit card (98%).

- Credit Card Statistics look at households in the 70th income percentile, which is now USD 118,438 when reviewing credit cards.

- Among ethnic groups, Asian Americans (92%) and Caucasian Americans (87%) are the most likely to have credit cards.

- In contrast, only 57% of households making less than USD 25,000 a year have a credit card.

Family Income | Percentage |

USD 100,000 or more | 98% |

| USD 50,000- USD 99,999 | 94% |

USD 25,000-USD 49,999 | 83% |

| Less than USD 25,000 | 57% |

Education | Percentage |

| Bachelor’s degree and more | 96% |

Some college/ technical or associate degree | 83% |

| High school degree or GED | 76% |

Less than a high school degree | 52% |

Race/Ethnicity | Percentage |

| Asian | 92% |

White | 87% |

| Hispanic | 73% |

Black | 71% |

- The number of people with credit cards has changed with age and tends to increase as they get older.

- Sometimes, having a balance is unavoidable. If you expect to carry a balance, getting a credit card with a 0% introductory APR can give you several months to pay off your debt without paying interest. Credit unions usually offer lower APRs, which can help you save on interest, according to Credit Card Statistics.

- In 2022, Gen Z members had an average of 2.1 credit cards, while Baby Boomers had 4.6. This is expected since people often open new accounts over their lifetimes.

Generation Z (18-25) | 2.1% |

| Millennials(26-41) | 3.4% |

Generation X (42-57) | 4.4% |

| Baby Boomers (58-73) | 4.6% |

Silent Generation (75+) | 3.4% |

(Reference: forbes.com)

- According to Federal Reserve data, 48% of credit card users had a balance at least once in 2022. While families with higher incomes were less likely to have a balance, many cardholders from all income levels still did.

- In 2022, 77% of US and US over 18 had at least one credit as per card Federal Reserve Bank of Atlanta.

- Credit Card Statistics stated that more than 75% of US households have at least one general-use credit card, as per CapitalOne.

- Credit Card Statistics, December 2023, found that 22% of credit cardholders are either somewhat or very unsure about paying their next credit card bill in full.

(Reference: forbes.com)

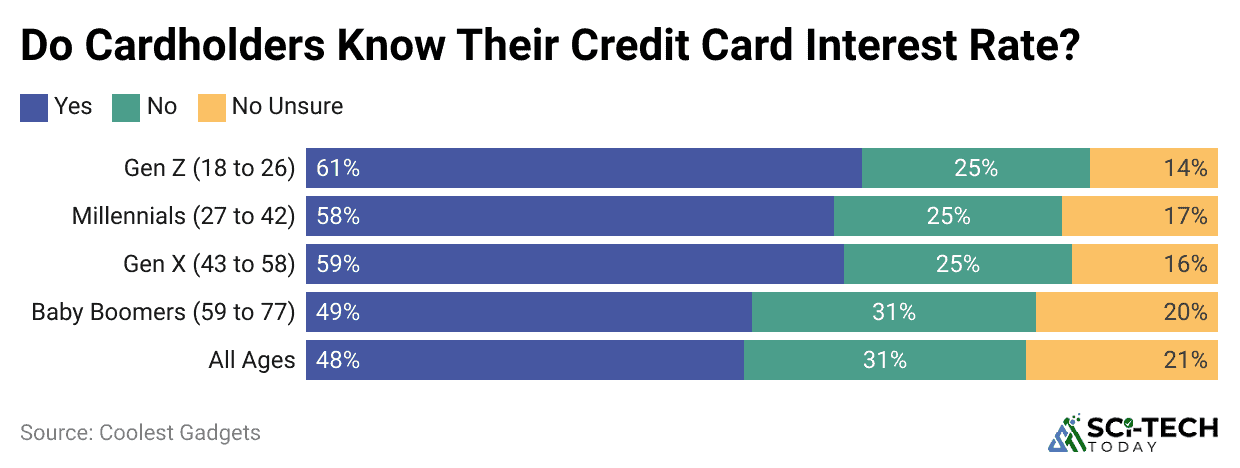

- According to Credit Card Statistics from December 2023, 46% of US credit card users need clarification or know their card’s interest rate. This uncertainty is common among all age groups.

- Since interest rates can change, credit card companies must give a 45-day notice before any rate adjustments.

- According to the Consumer Financial Protection Bureau, as of the end of 2021, 191.6 million out of 258.3 million adults in the US had a credit card.

- According to Credit Card Statistics, these 190.6 million cardholders use credit cards from around 4,000 issuers, four major networks, and various co-brand partners.

- Out of these cardholders, around 90 million have just a general-purpose credit card, 10 million have only a store-branded card, and 90 million have at least one of each type.

Types of Credit Card Interest Rate

- As of February 2024, the average annual percentage rate (APR) for credit cards with an outstanding balance was 22.63%, up from 16.98% in 2019.

- Credit card interest rates are partly based on the prime rate, which is connected to the federal funds rate. The current federal funds rate is between 5.25% and 5.50%.

- In recent years, the difference between the prime rate and credit card interest rates has widened.

- From 2013 to 2023, the average APR margin—the portion of a credit card’s interest rate not covered by the prime rate—rose by 4.3 percentage points.

- Credit card statistics state that interest rates also show differences based on race and ethnicity.

- In ZIP codes where most residents are Black, credit card rates were about 1.3 percentage points higher compared to ZIP codes with mostly white residents.

- Rates were about 1.4 percentage points higher in ZIP codes with mostly Hispanic residents than in majority-white ZIP codes.

The following are the types:

- Cash Advance APR: This rate is charged when you use your credit card to get cash from an ATM or bank.

- Penalty APR: If you miss a payment, a penalty APR may be added. This rate is higher than the regular APR, possibly up to 29.99%, but it usually returns to the normal rate after six months of timely payments.

- Purchase APR: This is the interest rate you pay on purchases if you don’t pay off your credit card balance completely each month.

- Introductory APR: Credit card companies may offer a special low rate, like 0%, to new users for a limited time after opening an account. This rate is lower than the regular APR.

- Balance Transfer APR: This rate applies when you move balances from other cards or loans to your credit card. Usually, there’s a low rate, or even 0%, for a few months before the regular APR starts.

Credit Card Regional Statistics

- New Jersey residents have the most credit card accounts, averaging 3.49 per person, according to Experian data.

- On the other hand, Mississippians have the fewest credit card accounts, averaging 2.57 per person. Interestingly, Alaska has the highest average credit card debt, according to Credit Card Statistics.

(Source: money.co.uk)

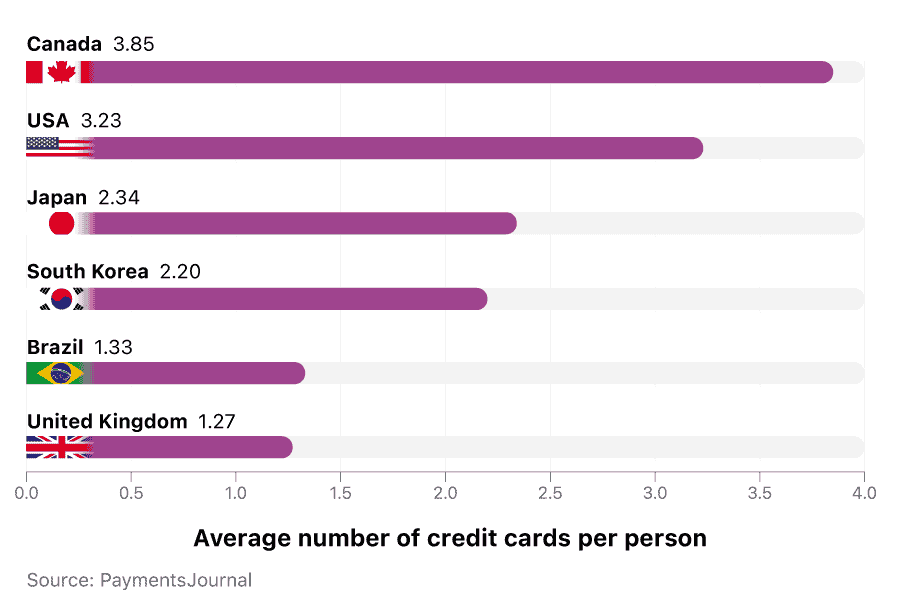

- The above chart compares the average number of credit cards per person in various nations.

Credit Card Statistics India

- In the financial year 2023, India had more than 2.9 billion credit card transactions worth over 14 trillion Indian rupees.

- This amount is expected to grow to over 58 trillion Indian rupees by the financial year 2028. At the same time, debit card transactions are projected to hit over 10 trillion Indian rupees by 2028, as per Credit Card Statistics.

(Reference: statista.com)

- In the financial year 2023, India had more than 2.9 billion credit card transactions worth over 14 trillion Indian rupees.

- This is expected to rise to over 58 trillion Indian rupees by the financial year 2028. The value of debit card transactions is projected to reach over 10 trillion Indian rupees by then.

(Reference: pwc.in)

- In the above chart, we can see the Credit Card insurance in millions between Mar 2017 and Mar 2026.

- In the last five years, India’s credit card sector has grown at a rate of 20% per year. By July 2022, over 78 million credit cards were in use.

- In May 2022, credit card spending reached a record USD 13.6 billion. Although spending increased overall, it grew only 9% during FY 2020F.Y.1 due to the COVID-19 pandemic.

- Credit Card Statistics also stated that the Reserve Bank of India (RBI) temporarily stopped some major issuers from issuing new cards.

- The rise of e-commerce, contactless payments, and market changes have significantly changed the credit card industry since the pandemic. Credit card issuance grew by 15% in FY 2022F.Y.

![]()

(Source: pwc.in)

- The above chart shows the credit card transaction for the years 2017 to 2026.

- However, 80% of the credit card market is controlled by the top six issuers. In the past three years, three new banks have started issuing credit cards.

- With ongoing changes, the industry is expected to grow nearly three times faster over the next four years.

- Transaction volume, value, and average spending on credit cards have all increased. For FY 2021F.Y.2, total credit card spending reached USD 139 billion, a 1.8 times increase from USD 77 billion in FY 2020F.Y.1.

- Credit Card Statistics stated that card transactions are expected to grow by 16% each year for the next four years. According to the RBI Payments Vision 2025, the number of card acceptance points will increase to 25 million, boosting transactions even more.

- The average transaction size has grown steadily by 7.3% after recovering from a dip in FY 2019F.Y.0, showing that more people are using credit cards for big purchases.

Credit Card Statistics United States of America

- Even with the recent decrease, credit card balances have still gone up by USD 259 billion since the end of 2021. Americans’ credit card debt is now USD 188 billion higher than the record of USD 927 billion set in the fourth quarter of 2019.

- Following are the top 10 highest average credit cards by state:

State | Average number of credit cards |

Maryland | 3.16 |

| Nevada | 3.18 |

Florida | 3.19 |

| Massachusetts | 3.21 |

Connecticut | 3.23 |

| Hawaii | 3.25 |

Rhode Island | 3.26 |

| New York | 3.34 |

New Jersey | 3.49 |

- Following are the top 10 lowest average credit cards by state:

State | Average number of Credit cards |

Kentucky | 2.78 |

| Tennessee | 2.77 |

Louisiana | 2.77 |

| Indiana | 2.77 |

West Virginia | 2.76 |

| Arkansas | 2.76 |

Oklahoma | 2.71 |

| Alabama | 2.69 |

Lowa | 2.67 |

| Mississippi | 2.57 |

- High interest rates, ongoing inflation, and other economic factors mean that credit card debt is likely to keep rising despite the recent drop.

(Source: lendingtree.com)

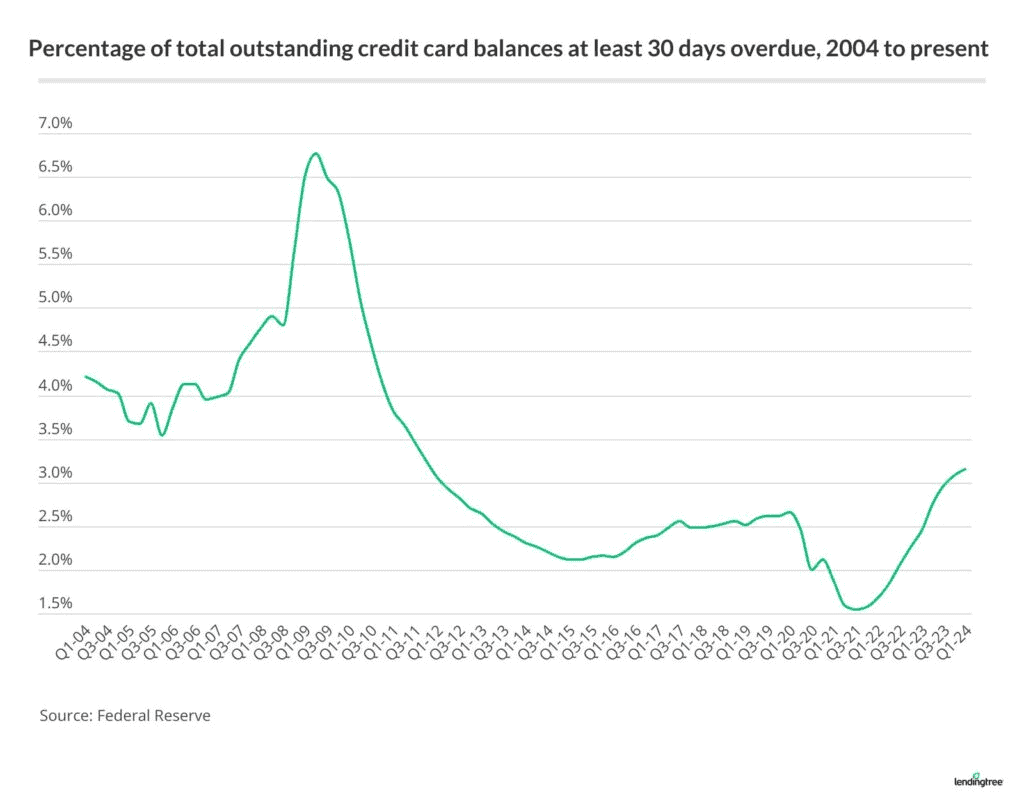

- The above chart shows the total outstanding credit card balance from 2008 to 2024.

- Among states, Oregon saw the biggest increase in credit card debt, with an average balance rising 7.8% from the third to the fourth quarter of 2023, going from USD 6,485 to USD 6,988. California (5.4%) and Massachusetts (5.2%) also had significant increases.

- Credit card debt increased sharply until the financial crisis in 2008 when it fell from USD 866 billion in late 2008 to USD 660 billion in early 2013. After that, according to credit card statistics, it started rising again.

- During the 2020 pandemic, credit card balances fell from USD 927 billion in late 2019 to USD 770 billion in early 2021. However, they went up sharply again in late 2021.

- On the other hand, Kentucky (14.0%) and Mississippi (12.4%) saw double-digit decreases. Arkansas (9.5%) and West Virginia (9.3%) also experienced notable drops.

(Source: lendingtree.com)

- According to the latest data from the Federal Reserve, the 30-day delinquency rate on credit cards—that is, the percentage of total balances that are at least 30 days overdue—rose from 3.08% in the fourth quarter of 2023 to 3.16% in the first quarter of 2024.

- This is the 10th consecutive quarter that delinquency rates have gone up, reaching the highest levels since the fourth quarter of 2011, when they were 3.25%.

- However, these rates are still relatively low compared to historical averages.

- Credit Card Statistics stated that the average delinquency rate since the Fed began tracking it in 1991 has been 3.73%, and it’s been 3.46% since 2000.

- Today’s rates are much lower than during the Great Recession when delinquency rates peaked at nearly 7% in 2009 and stayed above 5% for almost two years. Right now, only 3.16% of Americans’ total credit card balances are at least 30 days overdue.

Credit Card Statistics United Kingdom:

- In May 2022, 44 million UK adults (83% of the population) used some form of credit or loan. This is an 11% increase from 2017, when 39.6 million adults (78%) used credit, but a small drop from 2020, when 44.4 million adults (85%) used it.

- More than three-quarters (78%) of UK adults have at least one type of consumer credit, such as credit cards that are paid off monthly, down from 80% in 2020.

- Meanwhile, 17% of UK adults do not use credit, either by choice or because of their circumstances

(Source: money.co.uk)

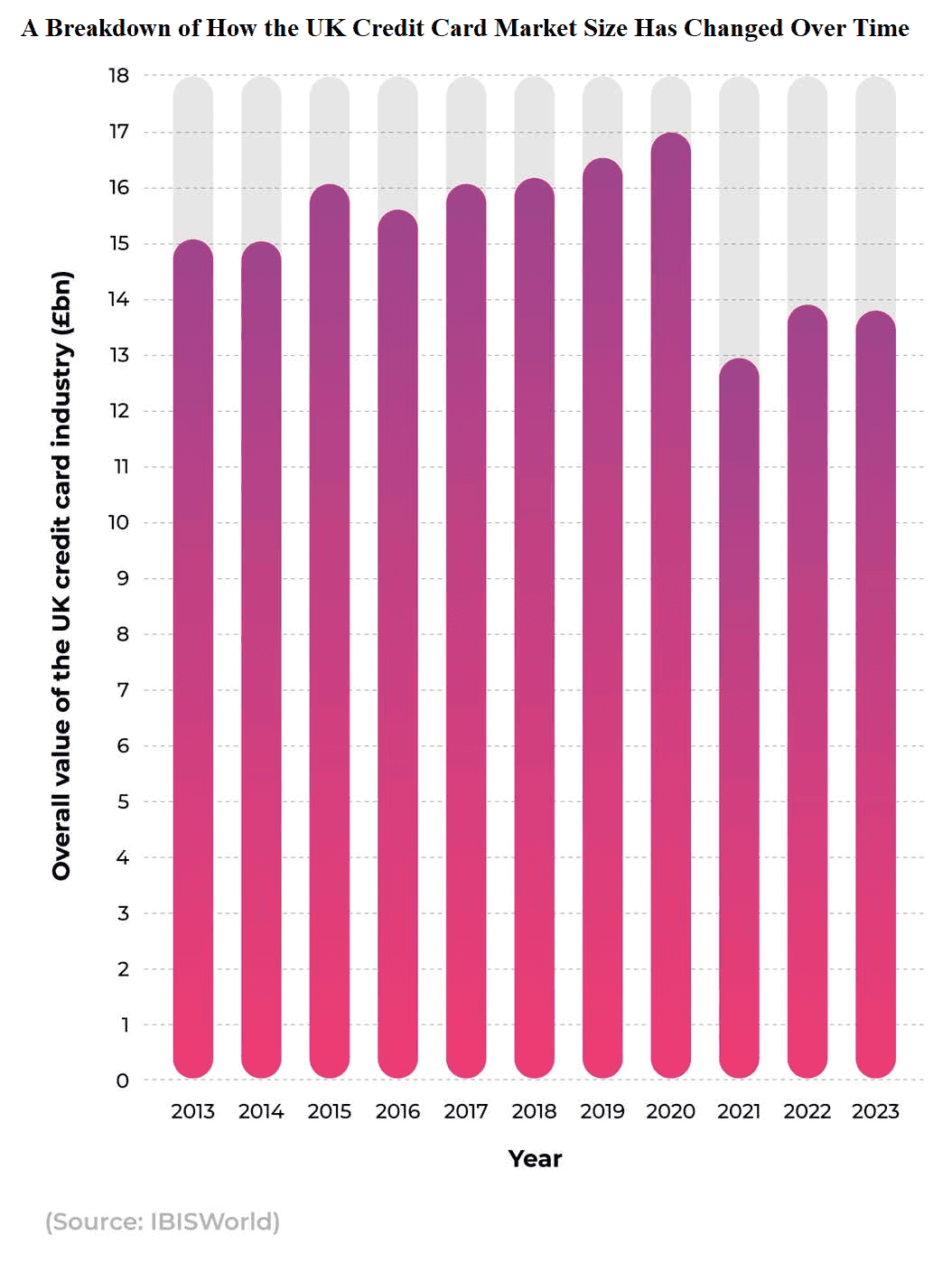

- In 2022, credit card issuance in the UK geneU.K.ted about £13.5 billion (USD 17.5 billion). From 2017 to 2022, the credit card market shrank by an average of 1.6% per year, but it grew by 4.9% in 2022.

- After an 8% increase between 2021 and 2022, the latest figures of £13.8 billion (USD 17.9 billion) show a small annual drop of less than 1%. This means the value of the UK credU.K. card industry in 2023 is about 19% lower than its peak in 2020.

- In the UK, 64% of adults (33.8 million) have at least one credit card. This is a decrease from 66% in 2020 but an increase from 62% in 2017.

- Credit card issuance in 2023 is estimated to have generated around £13.8 billion (USD 17.9 billion) in the UK.

- Kr steadily increased from 2013 to 2020, and the credit card industry saw a sharp decline of nearly 24% during the pandemic between 2020 and 2021.

(Source: money.co.uk)

- The average credit card balance in the UK has increased significantly in recent years. In December 2019, it fell from about £1,720 (USD 2,230) per month to just over £1,450 (USD 1,880) in May 2021.

- Since then, balances have steadily increased, peaking at £1,680 (USD 2,180) in April 2023. In May 2023, the average credit card balance was £1,675 (USD 2,170), which is 7.7% higher than in May 2022 and nearly 14% higher than in May 2021, as per Credit Card Statistics.

- The percentage of payments to balance stayed between 25% and 40% throughout 2020 and 2021, hitting 25% in June 2020 and 40% in October 2021.

- In January 2022, the percentage of payments to balance rose to 41.5%, and by May 2022, it was over 42%. Towards the end of 2022, this percentage started to drop, with the latest figure for May 2023 at 39.44%, down about 6% from the previous year.

Credit Card Network and Issuers Statistics

To identify the largest credit card companies, it’s important to understand what we mean by “credit card company.” For example, Visa, Mastercard, Citi, Capital One, and American Express are all credit card companies, but they have different roles:

- Credit Card Issuers are banks or financial institutions that manage card accounts. They handle applications and decide whether to approve or decline them. When you purchase with your card, you’re borrowing from the issuer, and when you pay your bill, you’re paying the issuer. Examples include Chase and Citi, as well as smaller banks and credit unions.

- Payment Networks are companies that process credit card transactions. The main networks in the US are Visa, Mastercard, American Express, and Discover. Visa and Mastercard don’t issue cards; they only handle transactions, while American Express and Discover do both.

- Lists of the biggest credit card companies often mix issuers and networks. The most common way to measure size in the credit card industry is by “purchase volume,” which is the total amount of money charged to credit cards.

Credit card data shows that:

- Visa has about 340 million credit cards in use.

- MasterCard has around 246 million credit cards.

- Discover issues about 57 million credit cards.

- American Express has roughly 53.8 million credit cards.

(Reference: enterpriseappstoday.com)

- By September 2023, ChChase’s purchase value was 32.8 billion, making it the leading issuer of general-purpose credit cards in the US and the top issuer of business credit cards in the country.

- In 2023, Chase issued about 149.3 million credit cards in the US.

(Reference: enterpriseappstoday.com)

- Visa has almost 52.8% of the credit card industry share globally.

(Reference: enterpriseappstoday.com)

- By this measure, the largest credit card issuer in the US isU.S.Morgan Chase.

- The global credit card market is expected to reach about USD 103.72 billion in 2023, representing a growth rate of 1.7 percent per year.

- According to Credit Card Statistics, by September 2023, American Express had a purchase value of USD 499 billion.

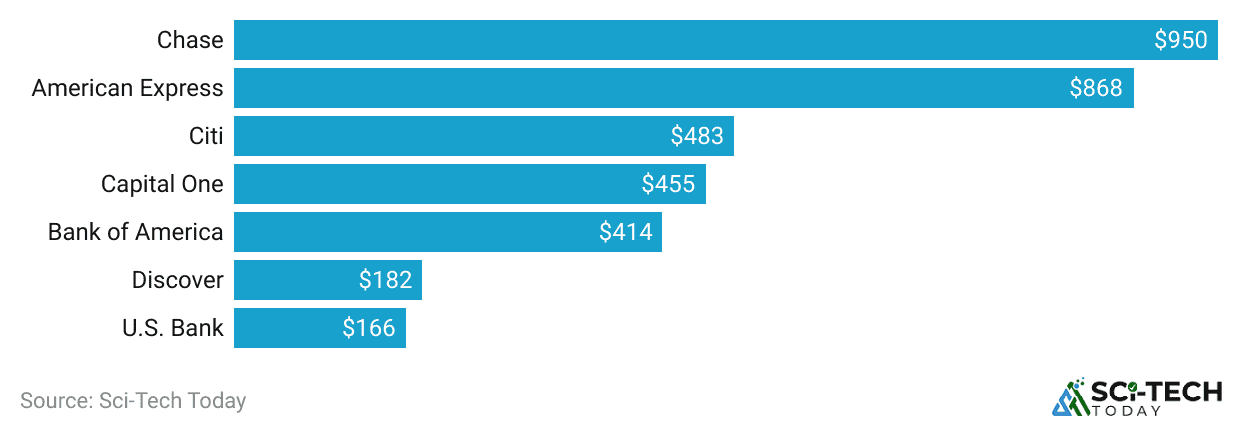

- Some of the top issuers of general-purpose credit cards include Citibank with USD 483 billion, Capital One with USD 455 billion, Bank of America with USD 414 billion, Discover with USD 182 billion, and US BankU.S.ith USD 166 billion.

According to the Credit Card Statistics, Chase cardholders charged USD 602 billion in the first six months of 2023. Here are the largest issuers by purchase volume during that time:

- JP Morgan Chase — USD 602.11 billion

- American Express — USD 547.56 billion

- Citi — USD 287.18 billion

- Capital One — USD 272.62 billion

- Bank of America® — USD 244.15 billion

- Discover — USD 105.82 billion

- U.S. BaU.S. USD 93.83 billion

- Wells Fargo — USD 90.56 billion

- Barclays — USD 55.16 billion

- Synchrony — USD 36.40 billion

- USAA — USD 28.07 billion

- PNC — USD 27.18 billion

- Corpay/Comdata — USD 25.50 billion

- Navy Federal Credit Union — USD 23.01 billion

- Wex — USD 21.87 billion

Most of these names are familiar. Less well-known names include Synchrony, which mainly issues store credit cards; Corpay (formerly Comdata), which provides corporate cards; and Wex, which issues specialty cards like gas cards for fleet businesses and benefits cards for employers.

- Different cardholders can have very different experiences with their card issuer’s customer service. One person might have a bad experience and rate the bank an “F,” while another might have a great experience and rate the same bank an “A+.” Despite these differences, some trends show up in customer satisfaction surveys.

- D. PoJ.D. conducts an annual study on customer satisfaction among major credit card issuers. According to J.D. PoJ.D.s 2023 study, American Express was rated the best credit card issuer for customer service. Here are the survey results:

Issuer | Score |

Credit One | 496 |

| Premier Bankcard | 529 |

Trust | 557 |

| Merrick Bank | 567 |

TD Bank | 572 |

| FNBO | 572 |

PNC | 574 |

| U.S. Ba | U.S.76 |

Barclays | 577** |

| Fifth Third | 584 |

Wells Fargo | 602 |

| Citi | 606 |

Chase | 607 |

| Issuer average | 609 |

Capital One | 616 |

| Discover | 629 |

Bank of America® | 629 |

| Navy Federal | 642** |

USAA | 647** |

| American Express | 657 |

Credit Utilization Ratio Statistics

- Your credit utilization ratio shows the percentage of your available revolving credit you are using.

- To find it, divide the amount of credit you’ve used by your total available credit. In India, lenders look at this ratio to see how well you handle your current debt.

- Lenders look at your credit utilization ratio to see how well you handle your current debt.

- To calculate it, divide the amount of credit you’re using by your total available credit.

- This ratio shows how much of your available credit you’re using and is key for lenders to judge your creditworthiness and financial responsibility.

- A healthy credit utilization ratio is generally considered to be below 30% of total available credit, according to Credit Card Statistics.

- For example, if your credit card limit is USD 20,000, try to keep your balance under USD 6,000 (30% of USD 20,000). Staying below this level shows you handle your credit well and can help boost your credit score.

Advantages and Disadvantages of Credit Card

Credit cards often get a bad reputation, but they can be very useful if used wisely. Here’s a simple look at the pros and cons of having a credit card:

Advantages

- Convenience: You don’t need to carry cash. Instead, you can use a credit card to pay for things. However, if you want to avoid debt, consider using a debit card. With a debit card, you spend only what you have in your bank account and don’t face high-interest charges.

- Recordkeeping: Credit cards provide a detailed record of your spending through monthly statements and online accounts. Some credit cards even send annual summaries that can help with taxes.

- Short-Term Loans: If you need to buy something now but will get paid later, you can use your credit card. Just make sure you can pay off the amount by the due date to avoid interest charges.

- Cash Advances: You can get cash from your credit card if you need it, but be aware that cash advances usually have higher interest rates. Make sure you have a plan to pay this money back.

- Rewards: Many credit cards offer discounts, cash back, or other perks based on your spending. Compare different cards to find one that matches your needs and habits.

- Build Credit: Using a credit card and paying off your balance on time helps build a good credit history. This can make it easier to get loans and credit in the future with better rates.

- Purchase Protection: If you need to dispute a charge or return a defective item, your credit card might help. Debit cards may offer similar protection, but you might have to wait longer to get your money back.

Disadvantages

- Temptation: Credit cards make it easy to spend more than you should.

- Interest Charges: If you don’t pay off your balance right away, you’ll end up paying extra in interest. This means your purchases will cost more over time.

- Fees: Some credit cards have annual fees or cash advance fees. High interest rates and fees might mean you spend more than you earn in rewards.

- Monthly Checking: You should review your credit card statement each month to ensure there are no mistakes or fraudulent charges. Credit cards can be targets for fraud.

- Temporary Low Rates: Some cards offer low interest rates for a limited time. Be sure to read the fine print, as the rate might increase later, leading to higher interest costs than you expected.

Conclusion

Many people think credit cards can lead to overspending, but if used wisely, they can help with bigger financial goals. Nowadays, people have more credit cards than ever, but they often use only about 25% of their credit limits because they’re cautious. There’s been a positive shift in how people use credit cards. Since the pandemic, average credit card balances have gone down as people reduce their spending. Credit card use is still widespread and will continue to play a big role in people’s financial lives.

Sources

FAQ.

The global credit card market was worth $489.4 billion in 2021. It is expected to grow from $521.8 billion in 2022 to $961.2 billion by 2030. This means the market will increase by 7.78% each year from 2023 to 2030.

The information displays the percentage of US consU.S.ers in different age groups who had a credit card in 2022 and 2023:

- Ages 18-29: 67% had a credit card in 2022.

- Ages 30-44: 79% had a credit card in 2022.

- Ages 45-59: 86% had a credit card in 2022.

- Ages 60 and older: 92% had a credit card in 2022.

In India, about 5.5% of the 1.4 billion people have credit cards, totalling around 77 million people. Even though this percentage is low, it represents a market larger than the entire population of Malaysia or Thailand.

HDFC Bank leads the credit card market. As of March 2024, it holds the largest share. Following behind are SBI Cards, ICICI Bank, and Axis Bank, with 19%, 17%, and 14% market shares, respectively, according to 1Lattice data.

60% of US and US cardholders have experienced fraud, and 45% have been defrauded multiple times. Last year, 52 million Americans had fraudulent charges on their credit or debit cards, with unauthorized spending totalling over $5 billion.

The annual percentage rate (APR) is the cost of borrowing money on a credit card. It includes the yearly interest rate you’ll be charged if you don’t pay off your balance each month, plus any extra fees. The APR can be different for each card. For example, one card might have an APR of 9.99%, while another might have an APR of 14.99%.

Interest charges are a big disadvantage of using credit cards. Credit cards usually have high interest rates, which can quickly increase your debt if you are not careful.

Saisuman is a professional content writer specializing in health, law, and space-related articles. Her experience includes designing featured articles for websites and newsletters, as well as conducting detailed research for medical professionals and researchers. Passionate about languages since childhood, Saisuman can read, write, and speak in five different languages. Her love for languages and reading inspired her to pursue a career in writing. Saisuman holds a Master's in Business Administration with a focus on Human Resources and has worked in a Human Resources firm for a year. She was previously associated with a French international company. In addition to writing, Saisuman enjoys traveling and singing classical songs in her leisure time.